Despite trading at all-time highs, Bitcoin’s implied volatility (IV) has collapsed to its lowest level in almost two years.

30-day at-the-money implied volatility for ETH (blue) and BTC (orange)

Source: Derive.xyz, Amberdata

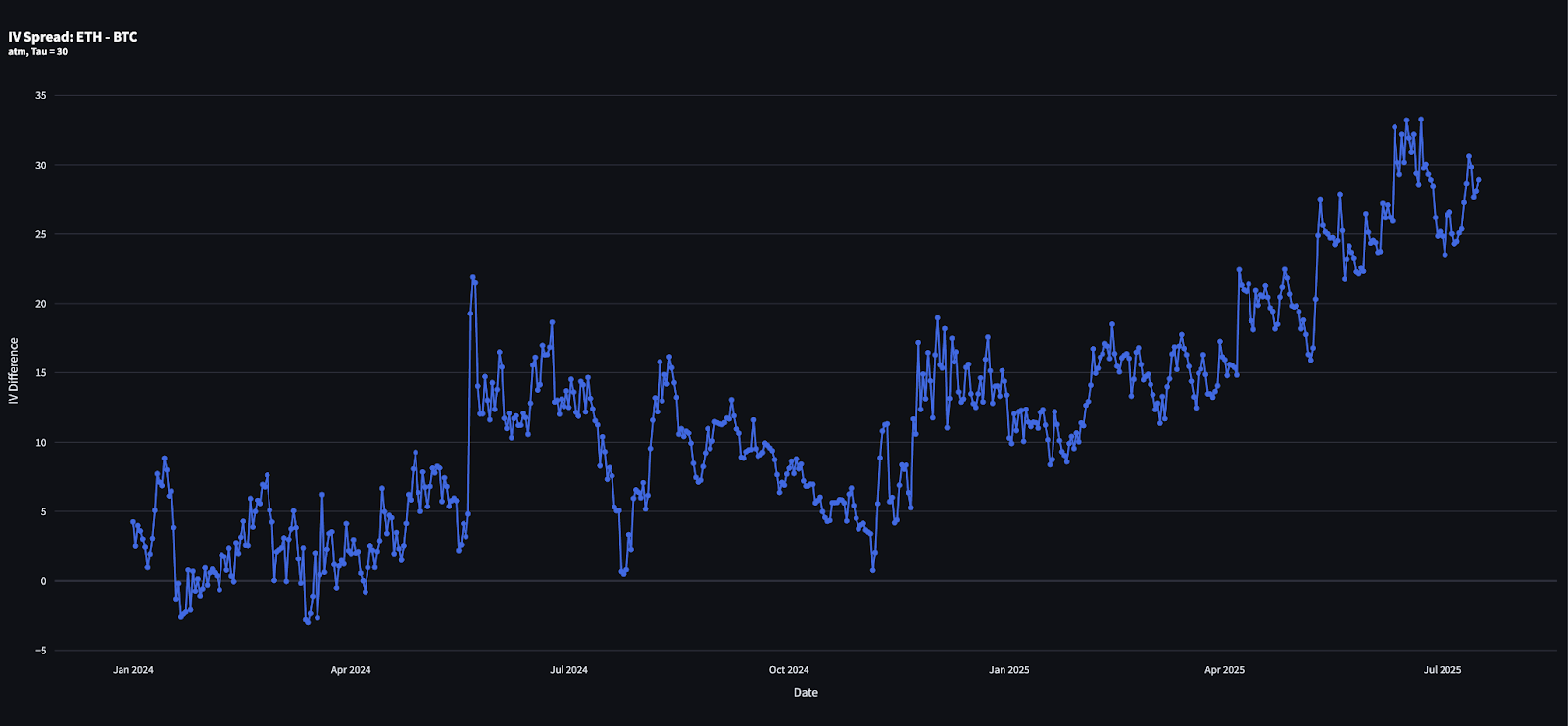

Meanwhile, Ethereum’s IV remains sticky and elevated, creating the widest divergence in BTC vs ETH volatility that we’ve seen in years.

Time series of the difference between ETH and BTC ATM volatility for the 30-day tenor between January 1, 2024, and mid-July, 2025

Source: Derive.xyz, Amberdata

So, why is Bitcoin becoming less volatile while Ethereum remains a lot more reactive? There are a few key drivers behind this divergence, starting with institutional participation.

Institutional flow

BTC adoption through ETFs is now roughly 10-times deeper than ETH’s. There’s $154 billion held in BTC ETFs compared to just $15.3 billion for ETH. As a result, BTC now enjoys deeper structural price support and a more mature derivatives ecosystem, both of which are contributing to lower realized and implied volatility.

On the derivatives side, around 22% of BTC futures open interest is trading on CME – a market dominated by institutions. For ETH, only 12% of futures OI is on the Chicago Mercantile Exchange (CME), which suggests retail still dominates ETH derivatives flows.

This institutional footprint in Bitcoin helps dampen volatility. More passive, long-term holders and less speculative trading leads to smoother price action.

Another factor is that a huge portion of BTC is now tied up in passive ETF structures. That reduces the amount of freely tradable supply and, as a result, reduces short-term volatility.

Ethereum, on the other hand, is still very yield-driven. ETH is constantly being looped through DeFi protocols, which are staked on Lido, restaked on EigenLayer, then split and sold for fixed yields on Pendle. Then that position is often levered again on lending platforms like Aave and Morpho.

This yield loop is great when things are going up, but it increases the risk of liquidations when things turn. That reflexivity is a key reason why ETH volatility stays high.

Bitcoin also has a unique suppressor in Strategy (MSTR). It has bought more than 226,000 BTC using convertible bonds, essentially embedding call options inside corporate debt.

These convertibles give institutions leveraged upside exposure to BTC without needing to bid up the crypto options market directly. At the same time, many of these investors hedge their exposure using futures and MSTR equity, which introduces mechanical hedging flows that further stabilize Bitcoin’s price.

There’s currently no ETH equivalent to this. We’re only now starting to see early-stage ETH strategy vehicles like Ether Machine, but they’re still small compared to what Michael Saylor has built with Strategy.

All of this suggests that Bitcoin’s collapsing volatility isn’t just a blip, it’s structural. It’s the result of growing institutional involvement, passive ETF inflows, and sophisticated hedging flows. Ethereum in contrast, remains speculative, yield-focused, and structurally levered, and that keeps volatility elevated. But in crypto, nothing stays still for long. We could see that structure shift quickly.

{kind=link}